Agendas

Here is the agenda of these posts. And more than you wanted to know about all sorts of agendas.

Here is the agenda of these posts. And more than you wanted to know about all sorts of agendas.

First post in a long series on Principles of Quantitative Development , on how an investment bank works.

On the loss of a second parent, and its implications.

After migrating to a Mac from a Time Machine backup, do you have missing events in your iPhoto library? Do not panic. Here is how to recover from the situation. Or better still, prevent it from happening..

Do you suffer from painfully slow Time Machine performance with your brand new Time Capsule? Here is how you solve it.

Take a quiz to see if you are an introvert or an extrovert – a techie or a manager.

On why I like to be quiet and keep listening to a world that can’t stop talking. It is prelude to an upcoming review of the book Quiet: The Power of Introverts in a World That Can’t Stop Talking by Susan Cain.

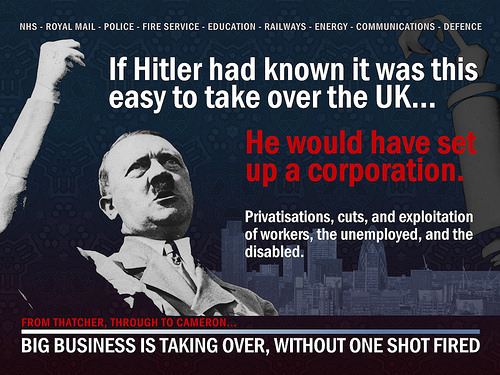

This article is a follow-up to my last post on what was troubling my conscience. This is also a rant on the modern capitalism of the corporate era, where we have all become tiny cogs in a giant wheel inexorably rolling on to nowhere in particular, but obliterating much in the process.

Do you feel troubled and responsible for things over which you have no control? If you do, this post may help you get by. Then again, it may make it worse…

When our kids turn 13, we turn ridiculous. How do we handle it?

A small anecdote to illustrate why one should stick to one’s language when arguing.